Let’s be honest fast food in our big cities just doesn’t hit like it used to. There was a time when grabbing a burger at McDonald’s, a slice at Pizza Hut, or a sub at Subway was a treat. It meant something. It was shiny, American, and aspirational.

Here’s the situation:

In Tier 1 cities, particularly in countries like India or rapidly developing economies, the demographic that once flocked to brands like McDonald’s or Domino’s for the novelty or aspirational value has evolved. These consumers now prefer:

Farm-to-table concepts Artisanal bakeries Third-wave coffee Craft burgers and gourmet pizzas Vegan/organic/keto/gluten-free menus And yes, bespoke fashion and curated dining experiences

The fast food model standardized, mass-produced, value-driven is struggling to remain culturally relevant among the upwardly mobile.

But things have changed. Fast.

Walk into any upscale neighborhood in a Tier 1 city today Mumbai, Bangalore, Delhi, Chennai and you’re more likely to find an artisanal sourdough pizza place, a gourmet cookie café, or a third-wave coffee shop with baristas who take their pour-overs more seriously than surgeons in an OR.

We’re eating differently now. We’re cooking differently. We’ve outgrown the chain mentality.

The Compressed Consideration Cycle (Survey Questionnaires)

And if the big names in fast food haven’t noticed, they’re in trouble.

The Data: A 2024 IIM Bangalore study found that 68% of Gen Z consumers discover new Quick Service Restaurant (QSR) outlets via social media. More importantly, 54% make a purchase decision within 24 hours of seeing a trending food video.

The Angle: Survey questionnaires distributed in Tier 2 markets consistently highlight this behavioral shift. This can be mapped directly to the prompt (socialismmedia content) is highly effective because the barrier to ability (digital access) has plummeted. The consideration cycle has collapsed from weeks to mere hours, meaning a physical footprint in a metro is no longer a prerequisite for driving intent.

The Fast Food Glow-Up… That Never Happened

Let’s call it like it is. Fast food didn’t evolve fast enough. It stayed frozen in time while its original audience moved on.

We’ve got bespoke tailoring, bespoke skincare, and yes bespoke dining. We want our food to be local, organic, fusion-inspired, Insta-worthy, and ideally with a story. A Big Mac just doesn’t cut it anymore when your neighborhood chef is fermenting kimchi in-house or cold-smoking jackfruit.

As Ryan Gosling said in Crazy, Stupid, Love (with Steve Carell in his dad jeans),

Be better than the Gap.

As rightly quoted from Crazy, Stupid, Love, the modern consumer wants brands to ‘be better than the Gap.’ Fast food, in its original format, is the Gap. It hasn’t evolved fast enough for Tier 1 cities that are flush with global trends and new money. The idea of ‘eating at KFC’ is now nostalgic, not aspirational.

We’re better than fast food now, too. At least in the cities.

The Economic “Push” Factor (Contextual Inquiry)

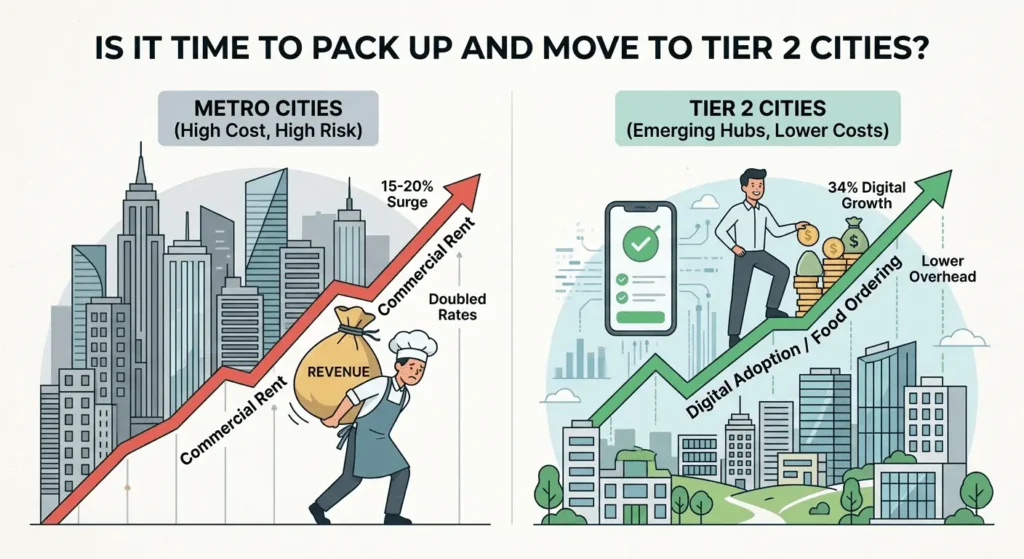

The Data: From 2024 to 2025, commercial rents in prime metro corridors surged by 15-20%. High-street locations in cities like Bangalore and Mumbai now demand upwards of ₹500 per sq. ft., doubling the rates found in Tier 2 cities. For some major chains, rent now eats up 12% of total revenue.

The Angle: The operational math forces a geographic move, but contextual inquiry in emerging hubs like Indore, Lucknow, or Coimbatore reveals the human side of the equation. Dining out in these cities is rapidly transitioning from a rare, special-occasion event to an everyday lifestyle choice. Lower overhead allows brands to reallocate capital into better service design and app experiences rather than just subsidizing expensive real estate.

Establishing the Trust Architecture (User Interviews)

The Data: Digital food ordering in India increased by 34% in 2024 alone, tracking with global trends where over 62% of all QSR orders are now processed through mobile apps and digital channels.

The Angle: Mass migration to digital ordering in Tier 2 cities isn’t just about localized UI; it requires building a robust trust architecture. Reflecting on the adoption hurdles of India’s early smartphone era, user interviews in semi-urban markets often reveal friction points around payment security and account creation. Emphasizing data minimalism and privacy by design in the checkout flow is critical for capturing high-frequency users in these regions.

So should these chains move to Tier 2 & Tier 3 cities or highways?

Yes, and many already are. Here’s why it makes business sense:

Opportunity: These cities still see fast food chains as a novelty. There’s brand equity there, and price points that align better with the lifestyle.

Urban Saturation: Tier 1 cities are saturated, not just with fast food chains but with competition from local startups doing gourmet food faster, better, and trendier. Real Estate Costs: High rents in city centers make ROI for fast food locations tighter, especially with declining footfall. Highway/Transit Locations: Strip malls, petrol pumps, transit stations, and national highways offer captive audiences, travelers, families, truckers looking for reliable, quick meals. Tier 2/3

Evolving User Motivations (Behavioral Observation)

The Data: It is a misconception that Tier 2 markets are strictly driven by price. A recent Deloitte/FICCI report noted a structural evolution where consumer demand in these cities is shifting heavily toward clean-label and protein-rich foods. Globally, nearly 48% of new QSR menu launches in 2024 featured health-conscious or alternative-protein options.

The Angle: This addresses the core ‘Motivation’ axis of behavior. A successful Tier 2 migration strategy must account for the fact that these consumers hold the exact same health-conscious aspirations as their metro counterparts, requiring menu architectures that balance affordability with quality signaling.

So Where Do They Go From Here?

If we’re being practical, the next obvious move for brands like McDonald’s, Domino’s, Taco Bell, KFC, and the like… is out. Literally.

Tier 2 and Tier 3 cities are ripe for growth.

In many of these cities, fast food is still cool. Still aspirational. Still a status symbol. It’s a safe, predictable option for families, students, and young professionals who might not have dozens of gourmet choices on Swiggy.

Highway strips, petrol pumps, and transit hubs are ideal.

Put a Taco Bell next to a Reliance petrol pump and you’ve got a captive audience : road-trippers, truckers, families, anyone wanting a break from mystery dhaba curries.

Cloud kitchens for the metros.

In Tier 1 cities, fast food can survive but mostly as a delivery model. Fewer dine-in locations, more smart kitchens slinging out fries and nuggets to nostalgia-driven millennials ordering from the comfort of their sofas.

They’re Not Dead But They’re Not the Moment Anymore

It’s not that fast food is irrelevant. It’s just… background noise now. Part of the landscape, but no longer the destination.

In Tier 1 cities, we’ve moved on. We want meaning in our food. Sustainability. Storytelling. Surprise.

If the chains want to stay relevant, they either need to completely reimagine themselves or gracefully exit the big-city spotlight and go where the market is still hungry for them.

Because in 2026, being ‘just good enough’ won’t cut it. Not with the new Indian palate. Not in our gated communities with organic farmer’s markets and charcoal lattes.

And certainly not when the guy next door is making sourdough pizzas that blow Pizza Hut out of the water.

Final thought: Fast food chains need to decide

Do they want to be part of the cultural conversation again or just chase volumes elsewhere?

Because Tier 1 city dwellers are asking for more than just food, they’re asking for experience, ethics, and elevation. And if the chains don’t pivot, the next-gen consumers will leave them behind… just like they left The Gap.