Architecting Trust & Financial Privacy in a High-Ambiguity Environment

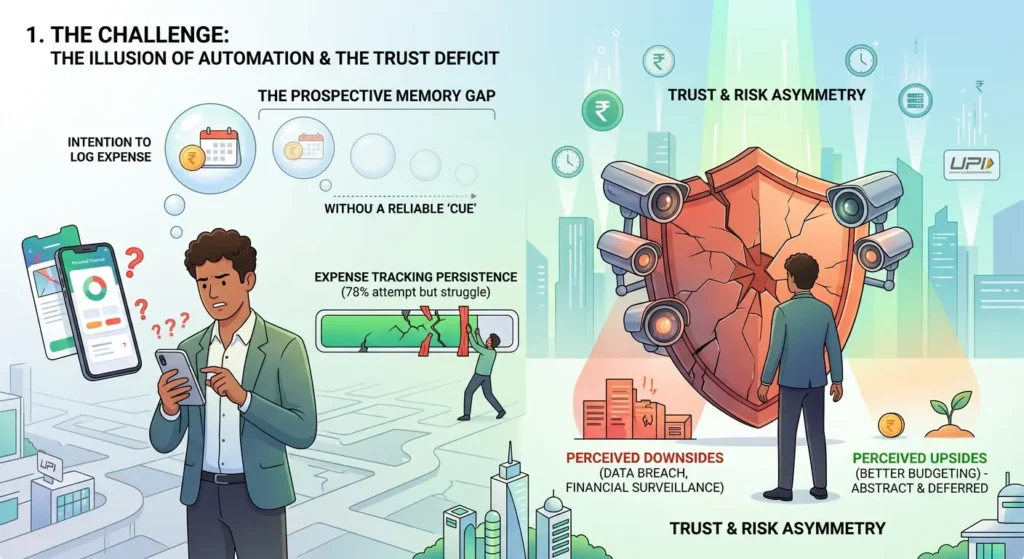

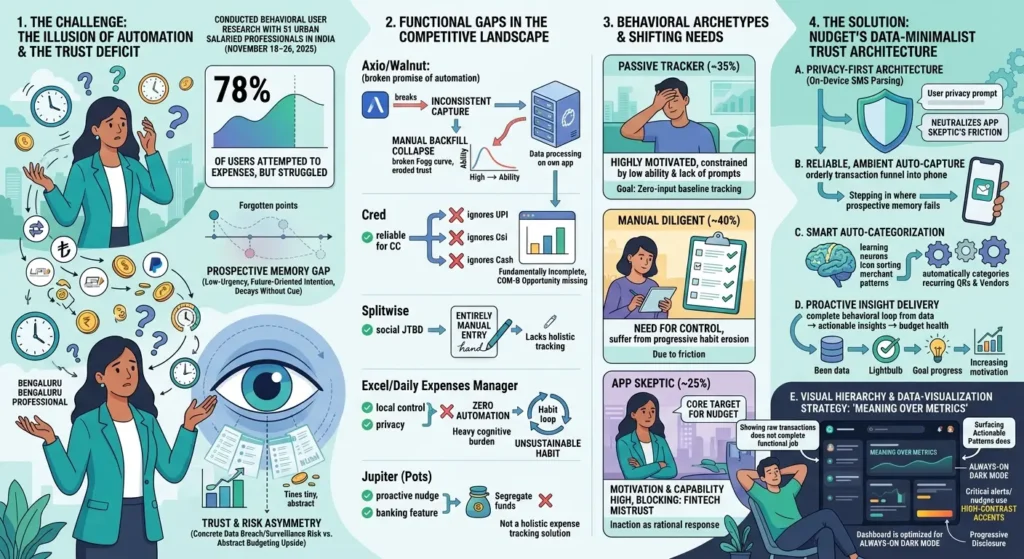

1. The Challenge: The Illusion of Automation & The Trust Deficit

In a UPI-first economy, personal finance management should be frictionless. Yet, user tracking behavior consistently fails. To understand why, we conducted behavioral user research with 51 urban salaried professionals in India between November 18–26, 2025.

The data revealed a high-ambiguity environment where 78% of users attempted to track expenses, but struggled to maintain the habit. The primary barriers weren’t just poor UI; they were deeply rooted psychological and structural roadblocks:

- The Prospective Memory Gap

Expense logging is a low-urgency, future-oriented intention. Without a reliable cue at the exact moment of a transaction, the user’s intention to track reliably decays. - Trust & Risk Asymmetry

For a significant segment of users, the perceived downside of an app (data breach, financial surveillance) is vivid and concrete, while the upside (better budgeting) remains abstract and deferred.

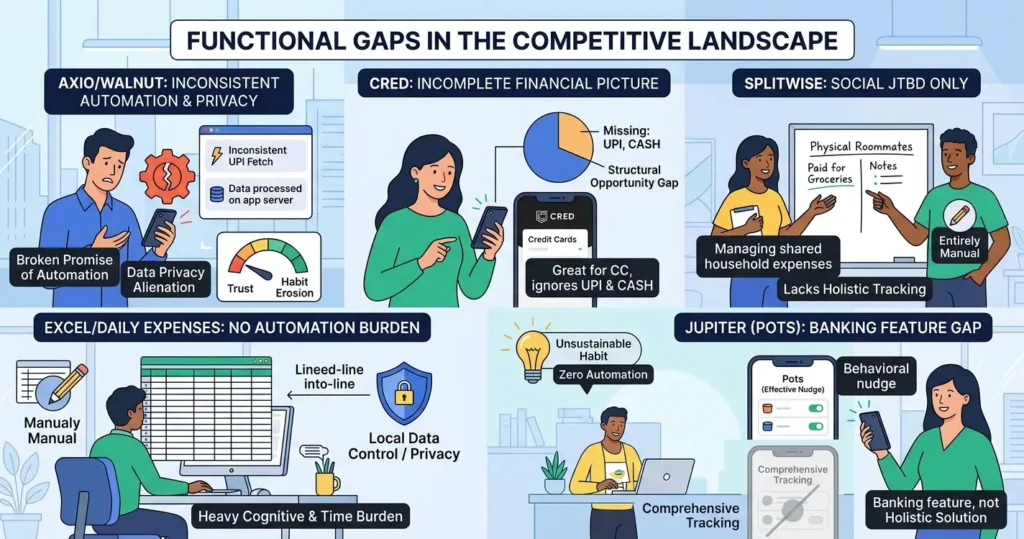

2. Functional Gaps in the Competitive Landscape

A friction mapping exercise of the existing ecosystem revealed that no single tool successfully balanced automation, actionable insights, and privacy.

- Axio / Walnut

While it attempts to automate UPI fetches, the capture is inconsistent. This broken promise forces users into manual backfill, triggering a collapse in the Fogg Behavior Model’s ‘Ability’ dimension and rapidly eroding user trust. Furthermore, data is processed on an app server, alienating privacy-conscious users. - Cred

Functions reliably for credit card tracking but completely ignores UPI and cash. This creates a structural ‘Opportunity’ gap (in the COM-B model), as it leaves the user’s financial picture fundamentally incomplete. - Splitwise

Successfully addresses the social Job-to-be-Done of managing shared household expenses, but requires entirely manual entry and lacks holistic tracking capabilities. - Excel / Daily Expenses Manager

These satisfy the user’s need for local data control and privacy. However, they offer zero automation. The heavy cognitive and time burden of manual entry prevents this from becoming a sustainable habit. - Jupiter (Pots)

Highly effective at providing a proactive behavioral nudge by segregating funds at the source to prevent misallocation. However, it is a banking feature rather than a comprehensive expense tracking solution.

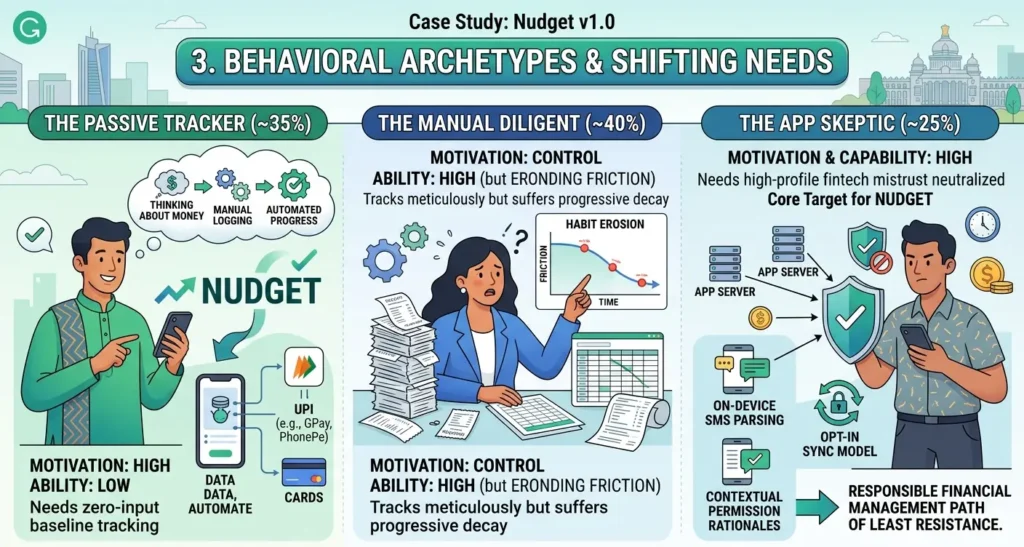

3. Behavioral Archetypes & Shifting Needs

Instead of relying on demographic personas, the research identified three distinct behavioral orientations:

- The Passive Tracker (~35%)

Highly motivated but constrained by a lack of behavioral prompts and low ability. They need zero-input baseline tracking to bypass their desire to not ‘think about money all the time’. - The Manual Diligent (~40%)

Motivated by a need for control, they track meticulously but suffer from progressive habit erosion due to the sheer friction of reconciling fragmented payment modes. - The App Skeptic (~25%)

The core target for Nudget. This segment has the motivation and capability to track but is blocked by high-profile fintech mistrust. Inaction is their rational response to intrusive permission requests.

4. UX Leadership: The Ethical Design Manifesto

To ensure Nudget didn’t slide into Dark Patterns, I authored a set of Ethical Design Guidelines to govern the MVP development.

| Principle | The Rule | The Why |

| Autonomy Over Automation | No automatic money movement without confirmation. | Auto-savings can cause overdrafts and loss of agency. We prioritize Intentionality. |

| The ‘Anti-Shame’ Directive | No judgmental language (e.g., ‘You failed’). | Shame leads to app abandonment. We use Positive Reframing (Opportunity Cost). |

| Friction Where It Matters | Intentional friction at the point of impulse spending. | We use Ethical Friction (a speed bump) to help the user align with their own long-term goals. |

| Relationship-First | If ‘Micro-policing’ is detected, trigger a ‘Health Check-in.’ | We are a relationship tool first, a finance tool second. |

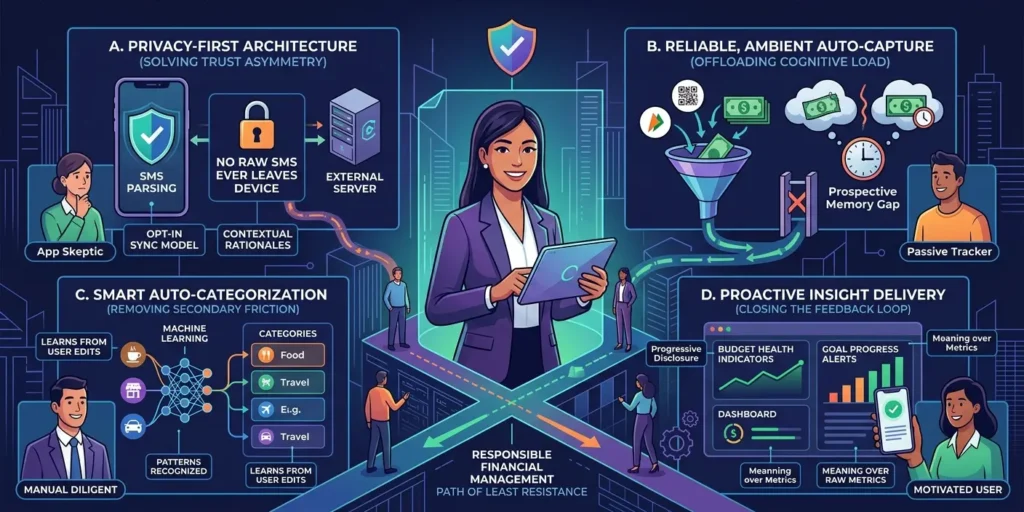

5. The Solution: Nudget’s Data-Minimalist Trust Architecture

To navigate these shifting user needs, Nudget was designed not as a better ledger, but as a behavioral system that makes responsible financial management the path of least resistance.

We focused on four structural interventions:

A. Privacy-First Architecture (Solving the Trust Asymmetry)

Privacy cannot be established through policy copy; it must be architectural. Nudget utilizes on-device SMS parsing, ensuring that raw financial messages are never transmitted to a third-party server. By implementing an opt-in sync model with explicit, contextual permission rationales at every request, Nudget neutralizes the App Skeptic’s primary friction point.

B. Reliable, Ambient Auto-Capture (Offloading Cognitive Load)

Because time was the universally cited barrier, partial automation was deemed worse than no automation. Nudget structurally changes the user’s environment by auto-capturing transactions locally, stepping in exactly where prospective memory fails.

C. Smart Auto-Categorization (Removing Secondary Friction)

Manual categorization imposes a heavy cognitive translation task on the user. Nudget replaces rigid, pre-defined category buckets with machine-learning-driven merchant pattern recognition. The system learns from the user’s edits over time, automatically categorizing recurring QR codes and vendor payments.

D. Proactive Insight Delivery (Closing the Feedback Loop)

Users expressed a clear Jobs-to-be-Done requirement: they needed to know what the data meant, not just what the data was. Nudget bridges this gap by delivering actionable insights such as budget health indicators and goal progress alerts to provide the automatic motivation required to turn one-time tracking into a sustained behavioral loop.

E. Visual Hierarchy & Data-Visualization Strategy: ‘Meaning over Metrics’

The core finding from the research is that users know what their goals are, but existing tools display data without meaning. Showing raw transactions does not complete the user’s functional job; surfacing actionable patterns does.

To satisfy the Passive Tracker’s need to not feel overwhelmed while maintaining the Manual Diligent’s need for control, Nudget’s dashboard relies on progressive disclosure. To reduce visual fatigue and maintain focus, the baseline aesthetic is optimized for an ‘Always-On’ dark mode, utilizing high-contrast accents exclusively for critical alerts or behavioral nudges.

6. The Impact & Looking Ahead: Closing the Loop on Trust and Automation

The initial design and release of Nudget v1.0 set out to prove a core hypothesis: privacy and automation are not mutually exclusive. By shifting the heavy lifting of expense tracking from the user’s memory to an ambient, on-device architecture, Nudget effectively bypasses the Prospective Memory Gap.

Furthermore, by making privacy an architectural guarantee rather than just a policy promise, Nudget neutralizes the deep-seated anxieties of the App Skeptic, transforming inaction into sustainable financial habits.

Defining Success: Key Behavioral Metrics

To validate these structural interventions, success for Nudget v1.0 isn’t just measured by downloads, but by habit persistence. We are tracking:

- Day-30 Habit Retention

Moving beyond the steep 7-day drop-off typical of manual entry ledgers like Excel or Splitwise. - Zero-Touch Categorization Rate

The percentage of transactions the ML model correctly categorizes without requiring the ‘Manual Diligent’ user to intervene. - Contextual Opt-In Conversion

Measuring the effectiveness of our progressive permission rationales in converting high-anxiety users into active trackers.

The Future Scope: Nudget 2.0 and Beyond

While version 1.0 successfully establishes a secure, automated baseline, personal finance is inherently dynamic. Future iterations will explore predictive budgeting, proactively nudging users before they break a behavioral boundary based on historical UPI patterns, and collaborative tracking to seamlessly blend individual privacy with shared household goals.

Ultimately, Nudget is designed with the understanding that users don’t want another app to manage; they want their cognitive load managed. By architecting trust into the very foundation of the platform, Nudget empowers users to focus on what their money means, rather than constantly worrying about where it went.